Summary

Senior Notes Mature 11/30/26 Yielding 9.5% with a 10.9% YTM.

My analysis on current business model suggests Argo needs just $14K BTC price to cover interest payments with current mining business.

Argo nears completion of Helios mining plant in Texas by end of 1H '22. Result will increase total hashrate greater than 2.4x.

Principal backstopped by crypto asset portfolio plus fixed investments.

Introduction

It's been a while since I had the time to share an idea for the income seekers on SA. Normally I would try to provide a more thorough presentation of the total company's business model, but my desire to share due to current pricing, and limited public data due to Argo Blockchain's (ARBK) very recent ADR OTC listing, makes it more difficult in this case. Hence, I strongly encourage everyone to do their own due diligence when looking at this security.

First, if you are generally predisposed against Crypto in general, then this article isn't for you. If you believe they are all worth zero in the future, then just move along. ARBK is a Crypto Miner. They have some elements that make them different from other public miners, but I'm not interested in those characteristics in this case. In general, I don't like equity investments in crypto miners. I view them essentially as similar to the assets themselves without much leverage in the model.

Thus, if you want to own the equity of ARBK, personally I'd suggest you should just own Crypto itself outright. You'll have similar upside without the exogenous risks that always come from owning equity in a company. If you're looking for leverage to Crypto prices, then there are better business models out there to invest in, like Silvergate Capital (SI) which I used to write about in '20-'21.

Instead, I'm interested in the recent issuance and decline of Argo's 8.75% Coupon Senior Notes due 11/30/26 (NASDAQ:ARBKL). I'm always looking for higher coupons specifically due to their lower convexity to interest rates. If you are concerned that rates will continue to climb higher due to inflation, then you either need to limit your duration, convexity, or preferably both through security selection.

ARBKL offers both of these aspects. The issue of course is that you have the opportunity due to the market's general aversion to this nascent industry. I don't consider this a table pounding opportunity. The Ramaco Resources (METC) Senior Note Issuance (METCL) was a better opportunity given our knowledge about near term results. Still, I think that the risk of ARBK not being able to cover the interest expense with EBITDA is low, which makes the current yield and yield-to-maturity look like an opportunity.

There are elements that make analysis difficult here though. First, this is a foreign entity domiciled in the UK with its primary stock trading on the London Stock Exchange. It's only been trading here in the U.S. since late September '21, which means we only have the Q3 '21 report that's been issued with USD stated numbers. Hence, the model I built I had to convert the British Pound figures using average exchange rates to convert into a USD model.

They are also using the proceeds of the debt issuance completed in November of '21 to complete the buildout of a very large new mining facility located in Texas called Helios. This will expand the total computing power, or Hashrate, from Q3 '21's end 1.075, up to 3.7 Exahash. That's over 2.4x times ARBK's current computing power that's estimated to come online in 2H of '22. Clearly the financials will change considerably once that happens, and the analysis I'm about to show you is based off of the last quarterly report. I.e., it's limited analysis! I wouldn't be sharing it though if I didn't think it might be worthwhile, so let's dig in.

Estimating BTC-USD Price and ARBK Cashflows

In the grand scheme of things the crypto mining business is a fairly simple model. Since we're focused on this debt security, however, we can make it even simpler and just focus on ARBK's ability to cover their interest expense payments first, and second their ability to return the principal capital when the issue matures. I'm going to ignore the potential variability that comes with the reward system for Bitcoin (BTC-USD) and other Proof-Of-Work networks. Instead I'm going to use their last reported quarter and try to answer one simple question: What price for BTC does ARBK need in order to cover their annual interest expense payments going forward? Or, how low can BTC's price fall before there would be a problem for debt holders?

The current 40 million of baby bonds were issued in November of '21 with a coupon of 8.75%. That requires 3.5 mil in annual interest payments until maturity. In the prospectus, ARBK provided the pro forma debt that is outstanding after the issuance and prepayment of 25 mil in the New Galaxy Term Loan. This leads to an increase of total debt to just over 70 mil from 57 mil at the end of Q3 despite the issuance of 40 mil. My usual conservatism is estimating 5% interest expense on the balance, so I'm going to use 5 million as the needed cash flow to cover total interest payments for all of their debt.

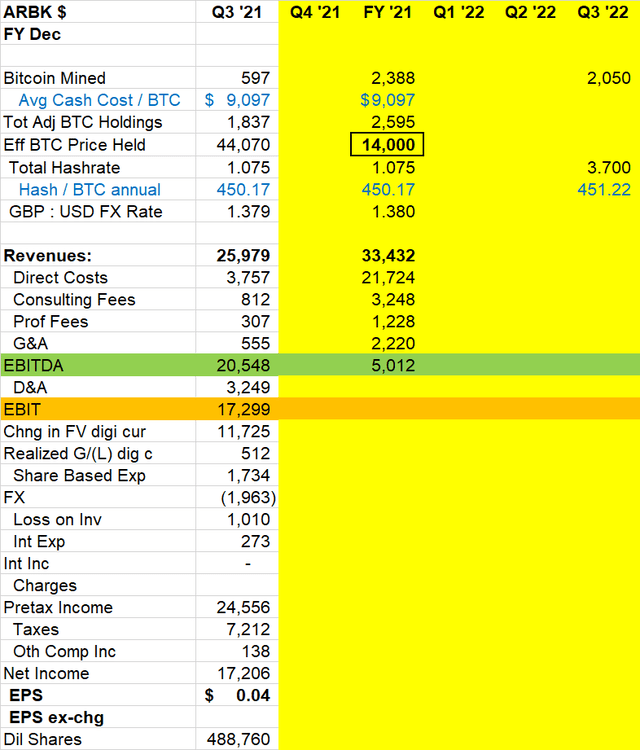

ARBK Income Statement (Company Reports)

Source: Company Reports

If you have looked at ARBK's reports before, then you'll notice I've adjusted the line items significantly from the company statements. Where ARBK has changes in the fair value of their held crypto assets above the operating line, I've moved it and anything else not related to the mining business below it. I want to estimate just what's needed for the mining business to cover the interest payments, and as you can see above the answer is about $14,000 BTC-USD.

This is just a test based off of Q3's results, and as the model shows their business is about to change dramatically in terms of the size of their mining operation. What we don't know right now is what their average cost will be per BTC mined in the 2H of '22. Still, I view $14,000 as a significant benchmark for what it suggests in terms of historical tail risk.

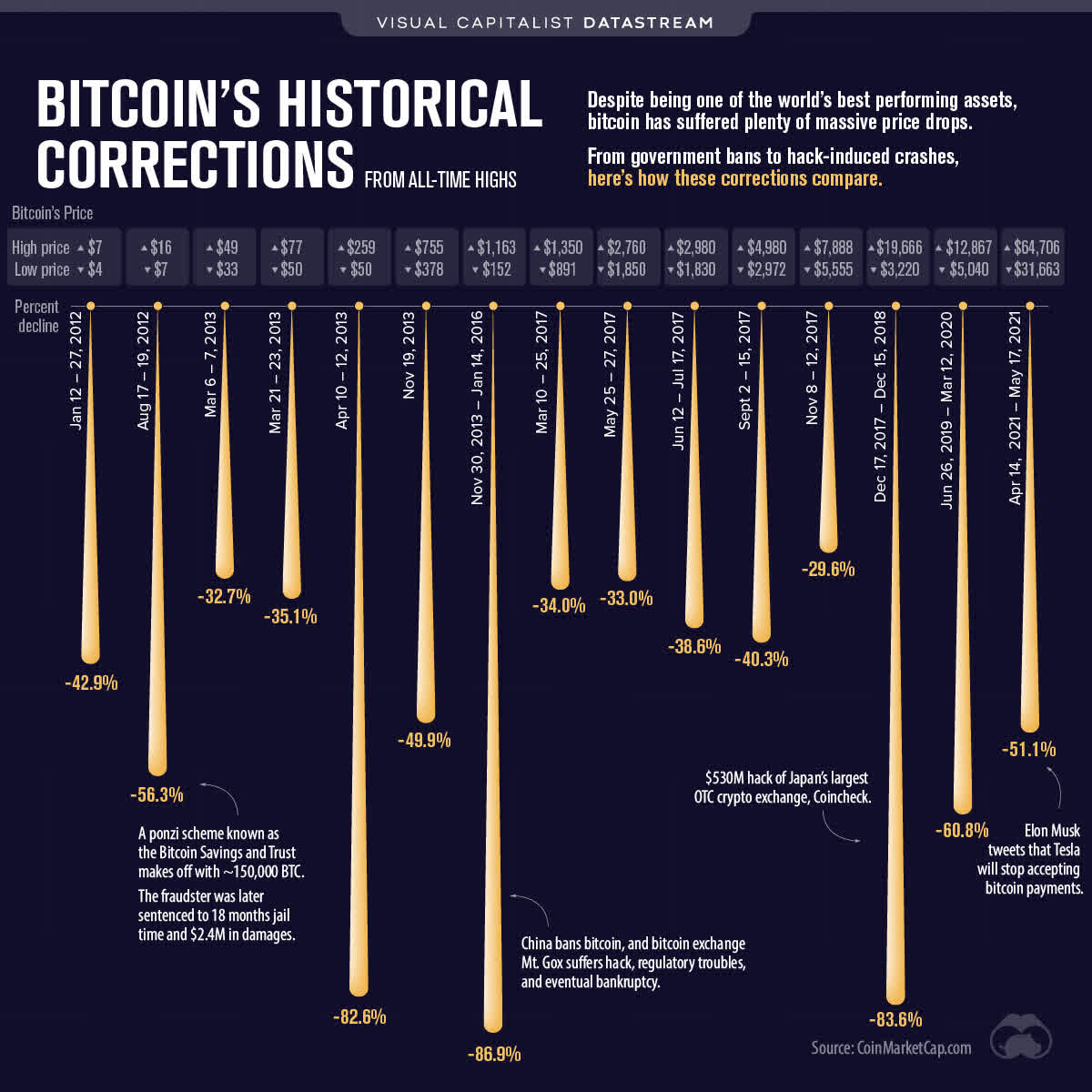

Visual Capitalist

The recent peak in BTC's price in November of '21 was about $69,000. Thus, a $14,000 figure would equate to a peak to trough decline of just under (80%). As the above chart shows, that's not a historical impossibility as we've seen three such declines of that magnitude in the past. One could argue that the magnitude of this kind of tail risk is likely less so than in the past due to the industry's growth and greater acceptance within traditional finance, however, we still have to accept this as at least a possibility although perhaps less of one. The fact that under current operating scenarios the mining business alone should be able to maintain paying the interest expense given even the greatest of market declines is why I find this an interesting security.

ARBK's Crypto Holdings

While I'm not interested in using changes in fair value of ARBK's crypto holdings to estimate the safety net for our debt securities, I do want to note that these assets help to effectively backstop the principal of our loan. In ARBK's most recent monthly update for the month of December, the company reported that they ended the year with 2,595 equivalent Bitcoins. Again, if we use that figure assuming no future growth in the holdings, ARBK would need a price of just about $15,400 BTC-USD to repay our $40 million in principal.

Lastly, there's also $100 million in Fixed Assets on the balance sheet that's mostly mining computers which will grow after completion of the Texas facility. Admittedly Bitcoin mining machines have to be constantly renewed, and ARBK depreciates those assets on a straight line basis for just 36 months. Still, if crypto prices plummet to the degree that inhibits ARBK's ability to maintain the business going forward, the current model as planned should have enough residual value to likely cover our principal return. That doesn't preclude the risk of ARBK adding on more debt etc., but we can only analyze what we now to be true right now. If circumstance change in the future, then we adjust our analysis accordingly.

Conclusion

One thing that I haven't done to this point is explain why this looks attractive to me in this market. For that I'd like to share a list of the current highest coupon offerings in the exchange traded baby bond market. The primary point I'd like to highlight is that all of these issues have a story for their capital raise. The next year estimates of EBITDA all expect a material ramp in the fortunes of these businesses.

That element requires depth of knowledge about each business to obtain the necessary level of comfort. I happened to have that with METC when they issued their debt, but I can't have that depth with every business in the market. Hence, what gives me greater comfort is when the current business can support the debt versus needing the expectation of next year's performance.

Disclaimer : The above empty space does not represent the position of this platform. If the content of the article is not logical or has irregularities, please submit feedback and we will delete or correct it, thank you!

COPYRIGHT © 2021-2025 HZD.COM ALL RIGHTS RESERVED